As an early-stage start-up founder, you are dealing with many different business issues simultaneously every day and working capital might not be high on your priority list. However, working capital is an important key to your company’s success.

Working capital is to your company as wind is to a sailing boat. You might drift along without it, trying your utmost best to row hard to avoid the rocks. However, to make good headway, you really need wind to provide that boost.

So, what is working capital in the context of finance and accounting? Working capital is basically the funds that you need to run your day-to-day operations. This affects many aspects of your business, from paying your suppliers to keeping the lights on. This sounds simple, but this is also one of the main reasons why a lot of start-ups fail.

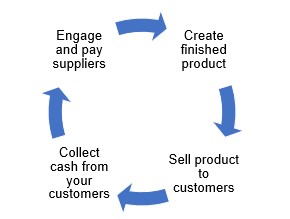

Think of this as a cycle:

To extract as much efficiency from the way you manage your cash, there are a few important ingredients that you will need:

- Collect cash upfront from sales (Receivable cycle): One way to do this could be to consider a small discount for customers who are willing to pay upfront for your product.

- Negotiate for favourable credit terms with suppliers (Payable cycle): Look to grow the relationships with your suppliers and hopefully they will be more flexible when it comes to prices and payment terms.

- Keep your inventory to as low as possible (Inventory cycle): You don’t want cash tied up in products that no one is buying!

The key to this is that you want to hold onto your cash longer and try to get paid quicker. This might sound easy on paper but executing this well in reality is complex. For start-ups that are dealing with large enterprises, conglomerates, and government entities, this gets even more complex as you are now dealing with longer payment terms.

This is an area where Genesis can come in to help to bridge this cashflow gap. Venture debt, when structured properly, can unlock capital earlier for your business to generate and fund new sales or investments, while minimising shareholder’s dilution. You can read more about venture debt here and the different types of loan structures here.

Managing your company’s working capital and cash flow in an efficient and effective manner is crucial for success, especially in the world of start-ups. Paying attention to these cash movements on your balance sheet will help you be a better founder and bring you closer to your goals. Let us work closely with you to understand your funding requirements.

If you have any questions, please get in touch with me.