Genesis Alternative Ventures raises US$125 million for second venture debt fund

Fund II welcomes new investor, Mizuho Bank, as Limited Partner

Former EDB Chairman Philip Yeo joins Advisory Board

Singapore, 10 Sep 2024 – Genesis Alternative Ventures has raised total commitments of US$125 million for its second Southeast Asia-focused venture debt fund.

Separately, Genesis and Indonesia’s digital-focused bank, Superbank, announced a collaboration in August 2023 to provide up to US$40 million of venture debt to promising technology start-ups in Indonesia. Superbank counts Emtek, Grab, Singtel and KakaoBank as significant shareholders.

Genesis also announced that Mr Philip Yeo, former Chairman of Singapore’s Economic Development Board, has joined Genesis’ Advisory Board. Mr Yeo is a veteran in the technology investment space across Southeast Asia and brings a wealth of experience and insights to guide Genesis’ continued growth and future strategies.

Dr Jeremy Loh, Genesis’ Co-Founder and Managing Partner, said: “We are grateful for the continued support of our limited partners and pleased to welcome new strategic institutional investor, Mizuho Bank, to Fund II. We are also delighted to welcome Mr Philip Yeo to our Advisory Board, a true statesman and visionary in the technology and investment space.

“Fund II has already deployed venture loans of more than US$20 million to a handful of promising start-ups across the region, including in Singapore, Indonesia, Malaysia, the Philippines. The current market has brought about a shift in start-up profiles, with a focus on leaner structures and a profitable mindset. Our portfolio companies exemplify this new direction, positioning themselves for long-term sustainability and success.”

Dr Loh added that while the start-up landscape presents its share of funding and exit challenges, Fund II has already marked its first successful warrant exit. “This validates the market demand for venture-backed companies that are strategically aligned with evolving market needs,” he said.

Yasuhiro Kubota, Managing Executive Officer and co-CEO for APAC, Mizuho Bank, Ltd., said: “We are delighted to come on board with Genesis on a shared vision in the venture debt space. Southeast Asia continues to be an exciting region with a thriving start-up ecosystem. We are confident that this partnership will accelerate the growth of promising firms with access to capital, industry networks and expertise led by Genesis.”

Genesis extends debt to revenue-generating companies that are backed by venture capital funds. These start-ups typically do not qualify for regular bank loans because they lack collateral, or have not yet reached profitability, and/or their founders and institutional investors are keen to take venture debt to build up the company’s credit worthiness while equally seeking to minimise unnecessary equity dilution.

About Genesis Alternative Ventures

Genesis Alternative Ventures is Southeast Asia’s leading private lender to venture and growth stage companies funded by tier-one VCs. Genesis is founded by a team of venture lending pioneers who have backed some of Southeast Asia’s best loved companies. Armed with a strong reputation among entrepreneurs and investors, Genesis is a trusted partner in empowering corporate growth while minimising shareholders’ equity dilution. Genesis was founded by Ben J Benjamin, Dr Jeremy Loh and Martin Tang in 2019.

Jakarta, Indonesia, 29 August 2024 – Eezee is excited to announce a groundbreaking partnership with Genesis Alternative Ventures (“Genesis”). This collaboration marks a significant milestone in trade working capital financing in Indonesia, aiming to bridge the gap between multinational corporations (MNCs) and small and medium-sized enterprises (SMEs), facilitating smoother and more efficient transactions.

Addressing a Critical Challenge

Many large MNCs in Indonesia face significant challenges in unlocking demand from SME suppliers. These SMEs often struggle with cash flow issues, which hinder their ability to meet procurement demands and offer necessary credit terms. Consequently, both SMEs and MNCs miss out on valuable business opportunities, stunting potential growth and economic progress.

An Optimal Debt Financing Solution

Through this strategic partnership, Eezee, alongside Genesis, can help bridge the working capital gap. MNCs can now conduct transactions via Eezee, backed by a committed debt facility from our venture debt partners. This financing model alleviates cash flow constraints for SMEs, eliminating the need for them to source external funds to meet procurement demands. By financing these transactions, we ensure that SMEs have the liquidity to seamlessly serve the procurement needs of large corporations

Empowering Indonesia’s SMEs

This debt facility is expected to make a substantial impact on the Indonesian market, empowering the country’s 62 million SMEs to focus on growth and innovation, tapping into previously unreachable demand from MNCs. This partnership aims to create a thriving business ecosystem where both SMEs and MNCs can collaborate to conduct business.

About Eezee

Eezee provides Global 2000 enterprises with procurement management solutions to manage their tail spend through our MRO industrial supplies marketplace and payment platform. Our platform, designed to work with third-party procurement and enterprise resource management software, enables businesses to pay vendors in “minutes” rather than weeks by cutting down on the administrative and operational challenges that come with engaging and paying vendors.

For further information on Eezee, please visit www.eezee.co.

About Genesis Alternative Ventures

Genesis Alternative Ventures is Southeast Asia’s leading private lender to venture and growth-stage companies funded by tier-one VCs. Genesis is founded by a team of venture lending pioneers who have backed some of Southeast Asia’s best loved companies. Armed with a strong reputation among entrepreneurs and investors, Genesis is a trusted partner in empowering corporate growth while minimising shareholders’ equity dilution. Genesis was founded by Ben J Benjamin, Dr Jeremy Loh and Martin Tang in 2019.

For further information on Genesis Alternative Ventures, please visit www.genesisventures.co.

Coffee is big business. With a market size estimated at $461.25 billion in 2022 and projected to expand at a CAGR of 5.2% from 2023 to 2030, it’s clear that coffee consumption is on the rise. The coffee market in Southeast Asia is projected to grow by 3.92% annually from 2024 to 2029, resulting in a market volume of

$10.3 billion in 2029. This growth reflects the region’s vibrant coffee scene, with consumers seeking unique experiences and emphasising sustainability and ethical sourcing.

Direct-to-consumer (DTC) brands are companies that generally bypass traditional retail channels to sell and market their products directly to consumers, typically through online platforms. The big idea is that this approach allows brands to have greater control over their marketing, customer experience, and pricing. The rise of e-commerce and digital marketing has fueled the growth of DTC brands, making it easier for startups and established companies alike to reach target audiences directly.

More and more, DTC brands have pursued an omnichannel approach in order to lay the foundations of sustainable business models. Many of the first movers in this space (think Warby Parker, Casper, Glossier etc) have already successfully integrated both off and online models.

Nowhere more clearly do we observe this trend than in the coffee space. Grab and go (GAG) coffee chains embrace a digital-first strategy to differentiate itself from traditional F&B businesses. The “New Retail” concept was put forward by Alibaba’s Jack Ma in 2016, which enables a seamless engagement between the online and offline world through data technology. A typical GAG coffee outlet has just enough space for the baristas to operate. There are limited seats (if any) and bare interiors. Smaller stores translate to lower rent and fewer employees. This significantly reduces each store’s operational costs, allowing chains to offer lower prices while maintaining a healthy margin. This leaner model also allows chains to expand more quickly. Customers can place their orders through the mobile app for pick up at their preferred outlet or delivery to their doorstep.

Coffee In Asia & Southeast Asia

Asia has already witnessed the emergence of a key pan-Asian home-grown coffee player – Jollibee Foods (JFC.PS) the region’s largest fast-food chain. Jollibee diversified into the coffee business through a series of acquisitions. Notably, in July 2024, Jollibee acquired a 70% stake in privately held South Korea’s Compose Coffee for $238 million. This followed their earlier acquisition of The Coffee Bean & Tea Leaf (CBTL) in 2019 for $350 million and a controlling stake in Vietnamese coffee chain Highlands Coffee in 2017.

Over the past five to seven years, the coffee landscape in Southeast Asia has undergone a remarkable transformation often with a strong flavour of technology (no double entendre intended) – download an app, get a first order at under $1 and receive your caffeine drink in 2 mins. Traditional coffee shops, boutique cafes and tech-savvy chains have sprouted up across the region, creating a vibrant and competitive market. From global giants like Starbucks and CBTL to homegrown unicorns like China’s Luckin and Indonesia’s Kopi Kenangan, coffee brands are vying for their share of the Southeast Asia market and consumer taste buds.

Figure 1: Top 10 Coffee Producing Countries in the World (Source: Biz Latin Hub)

Asia’s coffee consumption has grown by 1.5% in the past five years, compared to 0.5% growth in Europe and 1.2% in the U.S, according to the International Coffee Organization, turning the region into the coffee world’s soon-to-be center of gravity. Traditionally a tea-drinking region, Asia’s growing coffee consumption is largely driven by the rise of a middle class that is keen to try anything trendy.

Deeply rooted in their colonial past, coffee cultures and export prowess define Southeast Asian coffee scenes. Vietnam’s French influence and Indonesia’s Dutch heritage are evident in their brewing traditions. Both countries remain in the top five global coffee producers (Figure 1).

Mobile Platforms Shake Up The Market And Challenge Established Coffee Brands

Fueled by a burgeoning middle class with rising disposable income and a growing appreciation for specialty coffee, Southeast Asia is experiencing a coffee revolution of its own. This trend has given rise to a wave of innovative coffee startups that are disrupting the traditional market landscape.

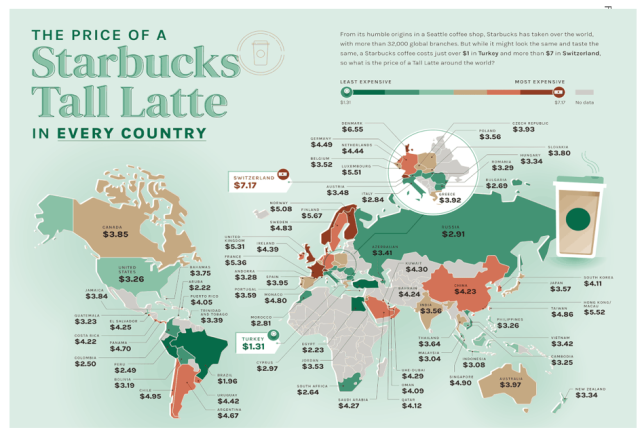

Price and unique flavour profiles are key drivers for many Southeast Asian entrepreneurs venturing into the coffee industry. Consider Starbucks’ pricing: a tall latte costs an American just 2% of their daily median income, but in Indonesia, that same drink can consume a staggering 30% of a local’s daily income (Figure 2). This vast disparity highlights the opportunity for homegrown coffee startups to cater to local tastes and offer competitive pricing model.

Figure 2: The Price of a Starbucks Tall Latte in Every Country (Source: Visual Capitalist)

While GAG chains thrive on digital efficiency and affordability, established brands like Starbucks are looking to bridge the gap with their own digital initiatives, recognizing the changing consumer landscape. Starbucks wants to be a welcoming space between home and work and hence, customer experience within the physical store is paramount. However, they also recognise the growing importance of digital integration.

In China, for example, Starbucks partnered with Alibaba to bridge the gap with competitors like Luckin Coffee. Through this collaboration, they leveraged Hema, Alibaba’s supermarket chain, to expand their delivery radius through “Star Kitchens” located within Hema stores. Following this success, Starbucks expanded its pre-order and in-store pickup options beyond its own app, integrating it with four Alibaba platforms like Alipay. This year, they further embraced the digital landscape by signing a regional partnership with Grab to enhance their reach within Southeast Asia

Kopi Kenangan, also known as Kenangan Coffee, has over 800 outlets and monthly sales of millions of cups. Their success hinges on a meticulously-crafted pricing strategy. Take the “Kopi Kenangan Mantan,” their signature iced latte with palm sugar, for example. At only Rp24,000 ($1.50), it is a steal compared to international chains. By offering locally crafted drinks significantly cheaper than Starbucks, they have tapped into a lucrative market gap without sacrificing profitability. This winning formula lies in an innovative retail concept: a seamless blend of small, convenient offline stores with robust online ordering services. This technology-first approach allows them to reduce operating costs and maximize profits for continued affordability. They are not alone in this game – companies like Jago Coffee and Sejuta Jiwa are all brewing up delicious and affordable options for the growing Indonesian market.

Photo credits: Revi Coffee Vietnam and Kopi Kenangan Indonesia

A Shot At Brewing Up Billions

VCs are bullish on the Southeast Asian coffee scene pouring significant funds into this burgeoning sector. The region’s consumer-focused startups grabbed the largest share of venture capital deal value last year, replacing software as the hottest investment destination. According to PitchBook’s 2024 Southeast Asia Private Capital Breakdown, $4.2 billion was invested in Southeast Asian B2C startups in 2023, a 31.3% increase from the previous year. It’s worth noting that this growth stands out – coffee was one of the few sectors to see a rise in deal value in 2023, and it represented a significant 36.5% of the total deal value for the region, its highest percentage since 2020.

This surge in VC interest translates directly to developments in the Southeast Asian coffee landscape. Coffee-related startups are a major driver of the D2C boom, offering innovative and convenient coffee experiences for a growing and discerning consumer base. Let’s explore some specific examples across the region:

Established Players with Big Brews: Indonesia boasts established coffee giants like Kopi Kenangan which has secured over $240 million in funding and achieved coveted unicorn status. Fore Coffee, another Indonesian player, is also a major player, having raised more than $40 million to date and offering a specialty coffee experience.

Emerging Players Brewing Innovation: New startups are brewing up excitement with innovative concepts. Malaysia’s Koppiku has secured $2.5 million, while Vietnamese tech-enabled coffee chain Révi Coffee & Tea, highlighting the growing appeal of Vietnamese coffee brands. founded by former Gojek executives, is making waves. Additionally, ZUS Coffee in Malaysia is reportedly preparing for a significant $53.5 million investment round. The Philippines with Grab-and-go Pickup Coffee raised $40 million and seeking to expand internationally into Mexico’s value-focused coffee market with an outlet in the Polanco neighbourhood of Mexico City.

Sustainable Solutions Sipping Success: VCs aren’t just focused on established models. Singapore’s Prefer, a startup offering bean-free coffee capsules for a more sustainable future, has secured $2 million in seed funding. This investment shows that VCs are looking beyond traditional models and towards innovative solutions that cater to the growing sustainability consciousness of consumers.

The surge in VC investment in Southeast Asian coffee startups translates to a plethora of choices for consumers. From established giants offering familiar comfort to innovative newcomers shaking things up, and sustainability-focused solutions for the eco-conscious, there’s something brewing for everyone. This fierce competition can be seen as a positive force, driving down prices and pushing boundaries in terms of service and product offerings. While some brands like Flash Coffee may not survive the intense competition, the survivors will be those that best adapt to consumer preferences and market dynamics.

An article written by Financier World Wide magazine. Read the full article here.

In the start-up world a variety of funding options exist for companies looking to foster growth or scale their enterprise. Among these options is venture debt financing – a form of financing that may not have the same visibility as other funding methods such as equity financing, but nevertheless plays a key role in the evolution of many start-ups.

“In recent months, activity in the venture debt market has demonstrated resilience and growth, with an increasing number of companies turning to this alternative source of capital,” says Jeremy Loh, co-founder and managing partner at Genesis Alternative Ventures. “There has been notable traction observed in venture debt financing deals, especially in Southeast Asia, where venture debt is still a relatively underutilised financing instrument.”

We were delighted to host our investors, partners, portfolio companies, and special guests for our annual Genesis LP Day at the iconic Raffles Hotel on 23 May 2024.

It was a fantastic gathering, filled with insightful discussions and a wonderful sense of community and we are grateful to overseas guests who travelled from Hong Kong, Indonesia, Korea, Japan, Malaysia, Thailand, and USA to join us

In addition to sharing about the performance of our Funds, our guests were treated to an insightful line-up of speakers:

Chin Hwee TAN (Energy Market Authority (EMA) Authority) explores the new multi-polar world in his latest book, “Economic Success: Fate or Destiny?” to the upcoming generation with the tools to understand and navigate this evolving landscape.

Ian Potter (Foundational Capital) on energy trends: “We’re adept at finding new ways to use energy, but less adept at finding new ways to produce it.” A thought-provoking perspective on the energy market’s future.

Bruno ROCHE (New Mutualism – The Economics of Mutuality) on responsible capitalism: Bruno offered valuable insights on the future of capitalism, emphasizing responsible business, sustainability, ESG, and mutual value creation. (Read his highly-recommended his book online for free here.)

The day continued with a Portfolio Showcase featuring six of our visionary founders who shared their aspirations and plans:

As a special thank you, we presented everyone with a unique gift: a pair of handcrafted porcelain teacups inscribed with 起源 (qǐyuán, meaning “origin”) and 创始 (chuàngshǐ, meaning “creation”). Each cup also features the Genesis leaf symbol, representing our shared commitment to cultivating growth and innovation, and ultimately, brewing a better future together.

Relive the afternoon’s highlights with our Recap Reel:

The equity winter is well underway and has impacted tech ecosystems globally. The catalysts behind this funding drought – rising interest rates, economic uncertainty, and a recalibration of valuations – are well-documented. While hopes for an imminent thaw remain, investors and start-ups have adapted to the new reality of longer and more difficult fundraising rounds with many companies choosing instead to cut costs, preserve cash, and raise bridge rounds from insiders until the equity market returns.

How has venture debt fared during this time? Have lenders been able to plug the gap or have they experienced similar trends? How did the collapse of venture lender behemoth Silicon Valley Bank (SVB) in March 2023 impact the lending ecosystem? Will venture lending developments in the United States (the undisputed market leader for venture lenders and borrowers) signal what’s round the corner for the Southeast Asia ecosystem?

We consider these questions and in parallel highlight key observations from Dr Jeremy Loh’s attendance at the second annual Venture Debt Conference held in March 2024 in New York (where Genesis participated in discussions and networking opportunities with the likes of prominent banks with venture lending businesses such as Silicon Valley Bank, a division of First Citizens Bank, HSBC, Deutsche Bank, Comerica and a spectrum of private debt funds ranging from dedicated venture debt funds like Runway Growth, Vistara Growth, Bootstrap Europe to private credit players such as Horizon Tech Finance.

Surprising Early Resilience Despite Headwinds

Figure 1: Data aggregated from PitchBook and Deloitte Tech and Media Predictions

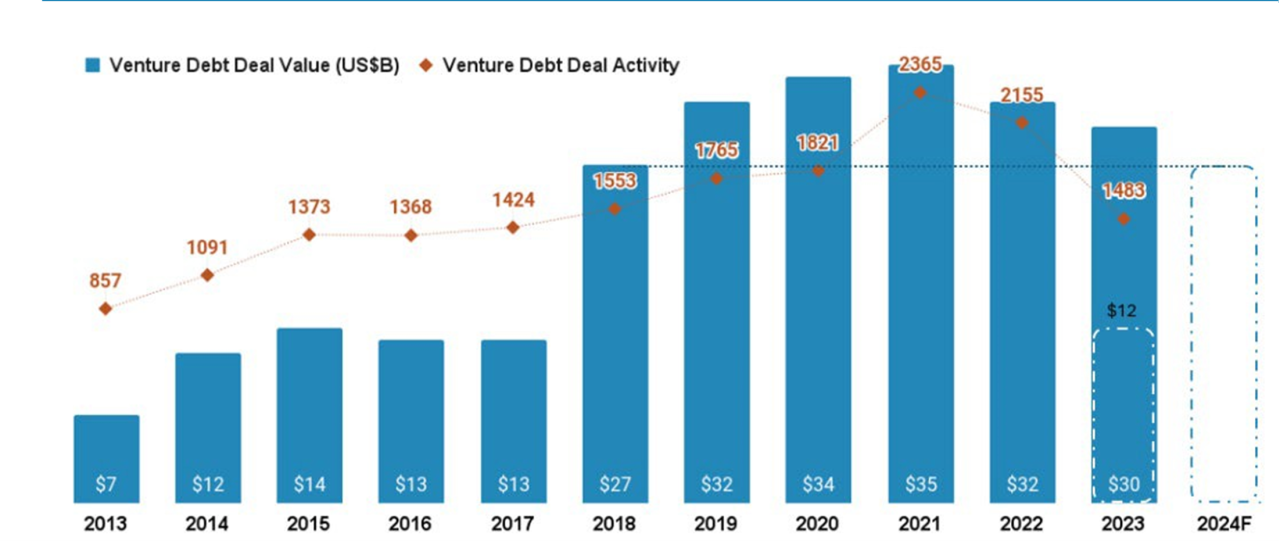

Market predictions following the SVB saga anticipated a significant decline in US venture debt financing for 2023. Forecasts suggested a potential drop exceeding 50%, ending a four-year streak of annual activity above $30 billion.

However, conference participants were bullish about venture debt pipeline opportunities. In fact, PitchBook data revealed a surprising resilience, with 2023 marking the fifth consecutive year surpassing the $30 billion threshold (Figure 1). Despite this positive development, a slowdown in capital availability within the venture sector is expected to impact 2024 figures. Estimates suggest a potential decline to a range of $14-16 billion but the outlier driving strong venture debt demand could push figures up to 2018 level of $27 billion.

A deeper analysis of venture debt deal count by startup stage sheds light on the allocation of venture debt capital (Figure 2, next page). PitchBook data indicates that seed and early-stage companies have experienced the most significant decline in deal volume. This aligns with the fact that SVB, which previously held a 50% market share in early-stage bank venture debt, has seen its lending shrink to roughly 20%. Conversely, late-stage loan activity has seen resilience and exhibited minimal decline, with 2023 emerging as the second-most active year in terms of deal count. Interestingly, PitchBook believes that there will be a continuation of the overall trend, predicting that venture debt in the US will exceed $30 billion for a fifth consecutive year in 2024. This optimistic outlook stands in contrast to the prevailing market sentiment, and only time will tell if it materialises when the first-quarter data of 2025 becomes available.

Figure 2: Venture debt loan count by stage

New Normal For Venture Debt: Proven Performers Welcome, VC Backing No Guarantee

The current economic climate has left many startups’ balance sheets in a less than ideal state compared to just a couple years ago. This tough environment has prompted investors and lenders to offer founders advice that may differ from what they’re accustomed to hearing. The message from Conference participants was clear: take the capital you can get – even if it’s at a down round with a liquidation preference – if that’s the only way to keep fighting.

Major venture and growth debt lenders are signalling a notable shift in their priorities. They are now open to financing established businesses with proven revenue models, even if they haven’t secured a recent equity round. In contrast, companies with dated equity rounds, limited traction, and a failure to reduce cash burn are the least preferred borrowers.

The focus for lenders has shifted to evaluating a company’s fundamentals – strong products, revenue generation, and a clear plan to bridge their funding gap. Profitability is seen as a major plus. Interestingly, the prestigious pedigree of a startup’s venture backers (e.g. Sequoia, Khosla Ventures) now carries less weight. As one lender put it, the key question used to be “Who’s backing you?”, but now a solid business case and financial runway are paramount in addition.

This evolving funding landscape requires startups to adapt their approach and messaging to appeal to the new priorities of investors and lenders. Those that can demonstrate financial discipline, revenue traction, and a clear path to profitability will be best positioned to secure the capital they need to weather the current economic storm.

Partnering With The Right Lender

When it comes to securing venture debt financing, the choice of lending partner is a crucial decision for startups. Considering that 76% of venture debt loans require amendments throughout their lifetime, startups must focus on finding a lender who can truly work alongside them as a strategic partner for the best possible outcome.

Lenders that take a “full platform approach”, tracking not only the financial performance of its portfolio, but also the holistic relationship and overall support provided to each company and founder are ideal partners. This level of commitment and consultative approach is key for startups navigating the complexities of the venture ecosystem.

Lenders with deep relationships within the venture capital community are also an important factor when choosing a reliable debt provider. These lenders are often involved in the debt raise conversation, providing valuable insights and alignment with the startup’s investors. Startups must be fully aware of the debt terms, such as meeting cash runway covenants, and understand the reporting requirements and third-party items demanded by the lender. The management team (and their key equity stakeholders) must be well-versed in navigating the positive and negative covenants.

Building trust and confidence in the counterparty relationship is paramount. Startups should seek lenders with a proven track record of working through challenging cycles and decisions alongside stable management teams. Forging these relationships proactively, and picking the lender’s brain on debt structure, can give startups an advantage. Creativity and sophistication in negotiations can also help bridge gaps, as the terms of warrants and other financing events can vary. Thorough due diligence is key, as startups can expect longer and more involved processes when selecting a venture debt partner.

Here’s a summary of the key points discussed by Conference participants:

Venture debt is more art than science – it’s crucial to find a lender that truly understands your business and the innovation economy;

Look for lenders with the right “Four Cs”: Capital, Commitment, Consultative approach, and Consistency through economic cycles;

Venture debt should be used judiciously, not as the sole source of runway – it needs to be part of a balanced financing strategy;

Startups must perform extensive due diligence on potential lenders, not just the other way around;

Venture debt can provide benefits like non-dilutive capital, runway extension, and acquisition/CAPEX funding – but the right lender partnership is key.

Navigating Venture Debt In A Challenging Funding Climate

As startups navigate the current funding landscape, the consideration of venture debt has become increasingly important. However, startups must approach this financing option with strategic foresight, balancing the benefits with the potential risks. In the current climate, the priority should be on securing access to capital and maintaining flexibility, rather than getting too caught up in the mathematical details.

One key factor to consider is the interest rate environment. While most lenders anticipate that interest rates will start to fall towards the mid-to-late 2024 timeframe, this could affect the repayment burden if rates are kept flat or for unforeseen circumstances begin to rise. This shifting rate landscape should factor into a startup’s decision-making process when evaluating venture debt.

Overleveraging debt can lead to negative outcomes, so startups must take the appropriate amount of leverage and have a clear repayment plan. Lenders view a “Hail Mary” situation as a red flag, so startups should aim to have a clear path to new equity or an M&A term sheet to make the venture debt more viable.

Companies seeking large debt raises may be a concerning signal, as it could suggest limited equity availability. Combining equity and debt can provide working capital and growth capital, but the management team must carefully consider and align with their board on the best approach.

Building strong borrower-lender relationships is crucial, looking beyond just interest rates. Startups should prioritize choosing lenders with specialized expertise in their industry and focus on cultivating a strong partnership, rather than solely optimizing for the lowest rate. Preparing quality financial statements in advance is also key, as lenders have become more sophisticated in their scrutiny. Startups should aim for audited financials, if feasible, to streamline the due diligence process and potentially facilitate deal-making.

In summary, navigating venture debt in the current funding climate requires startups to be strategic, discerning, and proactive. By carefully considering the trade-offs, building strong lender relationships, and ensuring financial readiness, startups can leverage venture debt to fuel their growth while mitigating risks.

Dealing with Distress: Lenders’ Approach to Troubled Startup Borrowers

When dealing with distressed startups that have raised venture debt, lenders must take a collaborative and pragmatic approach to achieve the best possible outcome. Despite any initial dissatisfaction, a successful workout requires all parties – lenders, management, and other stakeholders – to work together transparently and recognize the inherent value in the company’s assets.

Lenders should be proactive in identifying signs of financial distress, such as a startup’s failure to meet key milestones or its inability to raise fresh equity. When these issues arise, lenders should be upfront about their concerns and work collaboratively with the startup’s management to find a mutually agreeable financial solution that supports the company’s growth and path to cash flow positivity.

Employees and the management team are the primary stakeholders in a distressed startup scenario. Ensuring their motivation and satisfaction is crucial, as they are the ones who will ultimately drive the company’s turnaround efforts. Creditors must be willing to take a collaborative approach with management, even if it means accepting a less-than-ideal outcome for equity holders.

The concept of “management carve-outs” can be a useful tool in guiding distressed startups through this challenging period. In these situations, management teams may be unfamiliar with the complexities of insolvency and financial distress. Experienced general partners from the venture capital world can play a valuable role in helping management navigate these uncharted waters and align their actions with their fiduciary obligations to all stakeholders.

The emphasis is on having sponsors with strong track records and a proven ability to navigate these complex distress scenarios effectively. A single sponsor may be more efficient and have a distinct risk perspective, while a syndicate may face greater challenges in reaching consensus, potentially carrying slightly more risk.

While lenders must adopt a cooperative and pragmatic mindset, the key outcome is to maximize recovery. By prioritizing the needs of key stakeholders, leveraging management carve-outs, and maintaining transparent communication, lenders can increase the chances of a successful turnaround and maximize the value of the company’s assets

The Golden Age Of Credit: The Landscape Of Venture Debt And Bank Capital

Private credit as a broad asset class continues to attract significant fundraising dollars, with the venture debt category following suit and resulting in an ever-growing lending landscape. In recent years, there has been a notable compression in the cost of capital across various types of lending, including traditional bank facilities and venture debt. The increase in overall interest rates has led to a narrower pricing spread between these financing options, making bank capital more competitive in the current environment.

The emergence of larger, traditional investors exploring venture debt as an asset class has further validated its importance. For example, BlackRock’s acquisition of Kreos Capital, a European venture debt platform, highlights the growing prominence of this financing avenue. Kreos Capital has invested more than €5.2 billion through nearly 750 transactions across 19 countries since 1998. Another notable acquisition is Monroe Capital’s purchase of Horizon Technology Finance (NASDAQ: HRZN), a non-banking leading specialty finance company that provides venture debt financing. Monroe Capital, a $18.4 billion private credit firm with a 20-year track record in direct lending, has directly originated and invested more than $3 billion in venture loans to over 315 growing companies. These high-profile acquisitions by major players like BlackRock and Monroe Capital underscore the increasing significance of the venture debt market. The influx of larger, traditional investors validates venture debt as an attractive asset class, ushering in a “golden age” of credit with favorable conditions for investors.

In the aftermath of SVB’s collapse, major global banks have been jockeying to position themselves as the new preferred lender for startups globally. Institutions like JPMorgan Chase, HSBC, and Deutsche Bank have all made concerted efforts to capture this lucrative market. JPMorgan, for example, has been actively expanding its venture banking division, seeking to leverage its deep pockets and extensive resources to attract startups. The bank has touted its ability to provide comprehensive financial services, from lending to treasury management, to cater to the unique needs of high-growth companies. This trend has been driven by the increased capital formation within the venture capital community, allowing companies to stay private and grow for longer. As this trend reversed, leading to greater need of venture debt, traditional lenders have improved their underwriting capabilities to facilitate larger transactions.

Mature venture debt markets, such as the US and Europe, have demonstrated that both private venture debt funds and venture debt banks can coexist harmoniously. This provides startups with access to different lender profiles, allowing them to choose the most suitable option – a private lender with more flexibility in their lending criteria or established venture banks that provide tailored banking solutions. The coexistence of private venture debt funds and venture debt banks has proven to be beneficial for startups, as it provides them with a diverse range of financing options to support their growth and expansion plans.

In the burgeoning venture debt markets of North Asia, excluding China and India, Japanese banks have been actively establishing a foothold to lend to Japanese startups. Major players such as MUFG, Mizuho Bank, Aozora Bank, and Tokyo Star Bank have been aggressively pursuing opportunities in this space, recognizing the growth potential of the local thriving startup ecosystem. Over in South and Southeast Asia, HSBC recently announced the launch of a $1 billion ASEAN growth fund and a $150 million venture debt fund dedicated to the Singapore market. This followed two other $100 million HSBC single market venture debt vehicles – a MYR$500 (~US$104) million fund for Malaysia, and AUD$227 (~US$147) million fund for Australia.

The venture debt landscape in Southeast Asia is undergoing a transformative phase, driven by several key factors regionally and globally. Firstly, the region is witnessing a surging demand for alternative financing options, fueled by the burgeoning startup ecosystem and the need for capital to fuel growth. This growing demand has attracted competition from traditional banks and specialized venture debt providers, giving rise to co-lending opportunities, enabling lenders to collaborate and share risk.

These factors are collectively shaping the trajectory of venture debt as an alternative financing option in Southeast Asia’s burgeoning startup ecosystem. Private lenders, such as Genesis Alternative Ventures, are well-positioned to capitalize on this evolving landscape. As startups adapt to challenging market conditions and prioritize profitability, private lenders can continue to grow alongside the ecosystem, deploying debt financing to support lean, efficient, and profitable ventures.

The venture debt landscape in Southeast Asia is dynamic and rapidly evolving, presenting both opportunities and challenges for lenders and borrowers alike. Those who can navigate this landscape adeptly, balancing risk and opportunity while embracing sophistication and collaboration, will be poised to thrive in this exciting and promising market.

An article written by Gabriel Li (Vice President, Legal at Kredivo Group Limited) and Dr Jeremy Loh (Genesis Alternative Ventures) explains liquidation preference. Published by the Singapore Law Watch.

If you’re in the process of seeking equity financing or have done so previously, you’ve likely encountered the concept of “liquidation preference.” While online searches yield numerous articles providing a general overview, they often lack region-specific insights, particularly for founders seeking funding for a Singapore private limited company. This article offers a comprehensive introduction to “liquidation preference” within the Southeast Asia context, along with practical negotiation advice.

Jeremy Lee: Cleaning Up the Planet, One Tablet at a Time

Welcome back to the Genesis Founder’s Playbook series is a collection of curated insights and experiences from exceptional startup founders. Within this treasure trove, entrepreneurs share their valuable knowledge and hard-earned lessons with the startup community.

In our first Founder series for 2024, we spoke to Jeremy Lee who brings to mind the movie “Moneyball,” which based on the true story of the Oakland Athletics baseball team. In this movie, Billy Beane (portrayed by Brad Pitt) served as the general manager who built a winning team with limited resources. How? By challenging a player selection system that had proven effective for over a century but gives richer teams the upper hand.

SimplyGood, Jeremy’s latest venture, was born from his observation of the inefficiencies within the cleaning and personal care products sector, a domain largely monopolized by major FMCG players with established brands. Notably, these products, constituting a whopping 96% water, pose logistical challenges due to their bulkiness and weight during transportation. Moreover, they contribute to environmental pollution with their heavy reliance on single-use plastics.

Jeremy’s innovative solution offers consumers the essential cleaning ingredients in a dehydrated tablet form, creating a product line that is 200 times lighter and 300 times smaller than a conventional 500ml bottle of cleaning solution. This saves packaging, transportation, and logistics while reducing carbon footprint. Cost efficiencies are passed on to the end users, allowing them to clean without guilt.

Photo credit: SimplyGood

SimplyGood was born from his first venture, UglyGood, which he ran with a co-Founder during his university days. Driven by a commitment to sustainability and the circular economy, UglyGood ingeniously upcycled fruit pulp from local food manufacturers into valuable products such as animal feed, enzymes, and essential oils. Indeed one person’s waste is another’s treasure.

Now as a solo Founder who navigated SimplyGood through the challenging tech funding winter, he shares the following insights from his playbook:

++++

Jeremy’s journey in his own words:

Product-Market Fit is always a work in progress: When we launched SimplyGood, it was on the promise of eco-friendliness and sustainability. However, what we quickly realized was that while we had a small but very loyal following, it did not have broad-based appeal, making it difficult for us to scale. When we pivoted our messaging to convenience and value for money, we got a much better response. To date, more than 10,000 consumers have made the switch to SimplyGood. I don’t think our product-market fit is perfect yet and I believe it will always be evolving, rather than a one-time fix.

Listening to customers: We are very thankful to have customers who are very passionate about both sustainability and SimplyGood. Over the past few years, they have given us valuable feedback to improve our product design and customer journey, which we have incorporated.

Expansion through Strategic Partnerships: As a B2C business, I’m very mindful of the cost of customer acquisition (CAC). In the first year, spending a lot of marketing and brand building was inevitable as we were unknown. However, now that we have some brand awareness, we’ve expanded to B2B corporate partnerships, such as with property developers to provide starter kits for new home purchases, as well as business users like hotels, cleaning companies, and F&B businesses.

Balancing Sales and Brand Building: The conventional thinking is to build sales before brand building. However, I’ve discovered that tackling both simultaneously can open up new sales channels. Positioning SimplyGood as a sustainable and eco-friendly option has opened doors to collaboration with like-minded retailers. We are delighted to be chosen by MUJI Singapore to be part of their Sustainable Local Brands Project, and our range of products can now be found at their Plaza Singapura and Changi Jewel stores (at no listing fee!). Our products are also on the shelves at Commune Life stores, and we continue exploring partnerships with other retailers.

Support System: Having ventured into startup life first with a co-founder and now as a solo founder, I acknowledge the importance of a co-founder for emotional and mental support, even if it means a slower decision-making process. Therefore, I make it a point to connect with other founders to have a sympathetic listening ear and share experiences. I also take mini-breaks to rest and recharge.

People Matters: As a founder, I understand the multiple demands on our bandwidth. However, I think it is important to think about team and people management, especially if you want to scale. My experience has been to hire slow, but fire fast. As we are small and lean teams, wrong hires can adversely affect momentum, performance, and culture.

Tech Winter Survival Tips: In today’s uncertain fund-raising environment, founders should continue to focus on profitability, cash flow, and sound unit economics. Shifting our mentality from raising money to building sustainable businesses will serve us better in the long run.

+++

In the cleantech arena, Jeremy Lee stands out as a visionary force transforming sustainable living. He envisions a future where supermarket shelves are stocked cleaning tablets instead of the usual plastic bottles, aligning sound business sense with eco-friendliness and responsible consumption.

Feel free to reach out if you’re keen on contributing your own war stories to enrich the Founder’s Playbook and further strengthen our founder community. Together, we can build a network that thrives and succeeds.

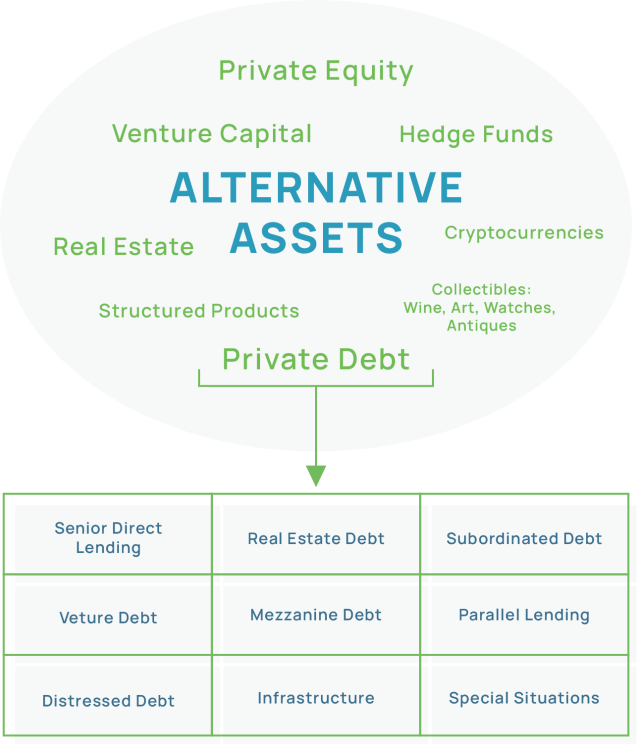

Private Debt has been grabbing headlines, with terms like Private Credit, Venture Debt, and Growth Debt often used interchangeably. However, it’s crucial to grasp the distinctions and understand the nuances. In this article, we unravel the intricacies of the overarching term “Private Debt” and focus on two key verticals – Venture Debt and Growth Debt – which are valuable financing tools for startups and scale-ups respectively.

Private Debt, a form of Alternative Assets, encompasses debt financing provided by private markets to companies outside traditional bank lending. Players in this arena include Debt Funds, Hedge Funds, Family Offices, Sovereign Wealth Funds, Non-Bank Financial Institutions, and Crowdfunding Platforms.

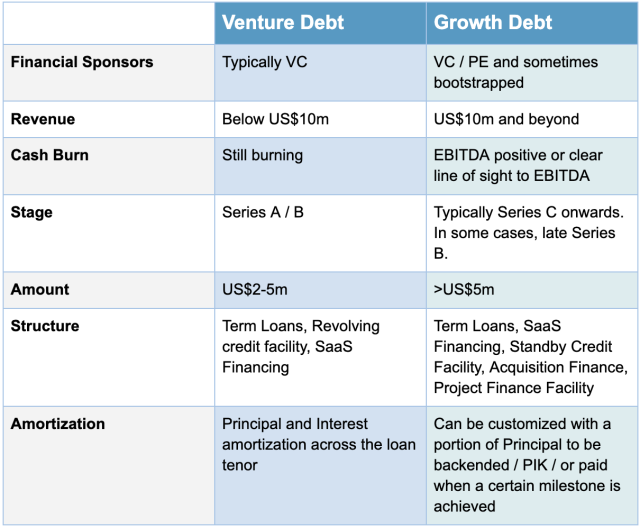

Venture Debt: Empowering Tech Innovators

Venture Debt is tailored for early-stage tech or tech-enabled companies (Series A and beyond). These companies, usually less than three years old, show high revenue growth, and have a unique/disruptive business model but are still burning cash. Venture debt has been a common financing tool in Silicon Valley but is still relatively new in Asia. Since Genesis first launched our venture debt fund five years ago, VC-backed companies in Southeast Asia have become more sophisticated about using venture debt as part of their overall capital financing strategy,

Venture Debt Structures: The Nuts and Bolts

Venture Debt typically takes the form of a term loan with a tenor of up to 36 months, repaid through monthly Principal and Interest amortization. Borrowers can access 20-30% of their recent financing round or cash on the balance sheet.

Reasons to opt for Venture Debt:

Filling working capital gaps for tangible outcomes, such as buying goods or raw materials.

Diversifying funding sources and reducing the weighted average cost of capital.

Minimizing dilution of early investors and founders across successive fundraises.

When to avoid Venture Debt:

Filling in for shortfalls or failures in equity fundraising.

The remaining cash runway is short and no other funding is available.

Funding Research and Development without a clear path to a commercial outcome.

Growth Debt: Fueling Expansion for Tech Titans

Growth Debt goes beyond Venture Debt by offering larger cheque sizes to mid to late-stage tech companies with revenues ranging from $10 million to over $100 million. Unlike Venture Debt, Growth Debt is not solely dependent on equity fundraising events and may serve as a substitute for equity. Examples of Growth Debt are Genesis’ loan to a leading global spatial data company before their IPO, as well as to Indonesian fintech firm, Akulaku. In essence, growth debt is a financing tool customized for later-stage startups who are hyper-scaling and preparing for an exit event.

Reasons to opt for Growth Debt:

Consolidating debt across entities or jurisdictions.

Refinancing costly or small quantum debt to benefit from improved terms e.g. lower interest rates or upsized debt.

Financing final rounds leading to profitability or pre-IPO stages.

Substituting for equity, reducing dilution for founders and early shareholders.

Funding projects with robust cash flows supporting debt repayment solely based on internal cash generation.

Acquiring an M&A target.

Credit Underwriting for Growth Debt: A Quick Overview

The credit underwriting process for Growth Debt is intricate, focusing on the company’s existing leverage, ability to achieve growth targets, reach profitability, and navigate market dynamics. Lenders assess the company’s attractiveness as a buyout or refinancing target, considering potential challenges to the original business case.

Comparing Venture Debt and Growth Debt: Key Distinctions

Venture Debt complements equity, emphasizing the fundamental quality of the borrower and its Financial Sponsors. Growth Debt at times may act as a substitute for equity, focusing on the company’s ability to execute growth plans independently and repay debt from internal cash generation.

The Genesis’ Approach: More Than Just Capital

Whether providing Venture Debt or Growth Debt solutions, Genesis takes a value-add approach, partnering with borrowers beyond cash. For insights on integrating debt into your fundraising plan or capital structure, we invite you to engage with us and explore the possibilities.

The table below outlines the differences and similarities between Venture and Growth debt.

For more information about Venture Debt and Growth Debt, please email us at contact@genesisventure.co.

Tough, challenging, economic headwinds, cautious optimism, interest rate hikes, downrounds, pay-to-play, layoffs – all these were words that startup entrepreneurs and venture investors became familiar with 2023. However, the year also saw several noteworthy developments that had a lasting impact on the venture capital landscape. We will address them in this quarter’s House View.

AI Ascending

2023 was a defining year for the Artificial Intelligence (AI) industry. AI became increasingly integrated into various industries, including healthcare, finance, manufacturing, and retail. Developments in machine learning, natural language processing, computer vision, and robotics were at the forefront of AI advancements. These technologies were driving innovation across sectors. Businesses leveraged AI to improve efficiency, customer experiences, and decision-making processes. Large tech companies continued to acquire AI startups to enhance their AI capabilities and expand their market presence. Microsoft became a leader in AI adoption with close integration of ChatGPT into its Bing search engine since announcing a $10 billion investment in OpenAI, the creator of the ChatGPT chatbot. What is exciting is the combination of the power of large language models (LLMs) with data in the Microsoft apps to turn words into the most powerful productivity tool on the planet. But as AI adoption grew, there was also a growing focus on ethics and regulations surrounding AI applications, particularly in areas like data privacy and algorithmic bias.

Silicon Valley Bank Collapse

One of the most notable events of 2023 was the sudden collapse of Silicon Valley Bank in March, a venerable institution that had long been synonymous with the technology and innovation hub of California. Its downfall sent shockwaves through the startup ecosystem, serving as a stark reminder of the fragility that can underlie even the most established financial institutions. In the aftermath of SVB’s failure, startups and venture capital funds faced not only the practical challenges of disrupted financial operations but also the psychological impact of shattered trust in financial institutions. This event served as a critical lesson in risk management and diversification, reinforcing the need for resilience and adaptability in the ever-evolving landscape of the startup and venture capital world. It also highlighted the importance of contingency planning and the necessity of spreading financial risks across multiple trusted partners to safeguard the interests of all stakeholders.

End of IPO Ice Age?

The IPO market remained frozen throughout 2023, save for a few iconic listings like Arm, Instacart, and Klaviyo, depriving startups of a traditional exit strategy and forcing them to reassess their growth trajectories. Courier startup J&T Global Express, which launched in Indonesia before expanding across Southeast Asia and China was valued at $13 billion in its Hong Kong IPO, below its last private round valuation of $20 billion as reported. Singapore’s first SPAC, VTAC, listed in January 2022 and backed by Vertex Venture Holdings, the venture capital arm of Singapore’s sovereign wealth fund, Temasek Holdings. VTAC merged with Asia’s live streaming app 17LIVE to take the startup public on Singapore’s stock exchange in December 2023.

What could be the catalyst that rekindles the interest in tech startup IPOs? First and foremost, a resurgence of confidence in market stability is essential. Renewed assurance that market volatility could be normalizing may set the stage for increased IPO activity. Furthermore, decisions made by the US Federal Reserve and other central banks concerning interest rates will wield considerable influence. These decisions ripple through the technology sector, impacting future cash flows of companies, driving valuation rebounds, and shaping investor sentiment. The current challenging capital market conditions present an opportune moment to lay the groundwork for an IPO, especially considering that the preparation process typically spans 12 to 18 months. Commencing preparations today positions companies to be fully prepared when favorable market conditions eventually return. On the 2024 IPO pipeline watchlist are some exciting candidates, including OpenAI which saw a leadership drama cutting its valuation down to $50B, Stripe – the Fintech payment darling that played a key role in disrupting the payments world with an estimated $50B valuation and Canva, the Adobe competitor with a potential $10B valuation.

From Setbacks to Comebacks

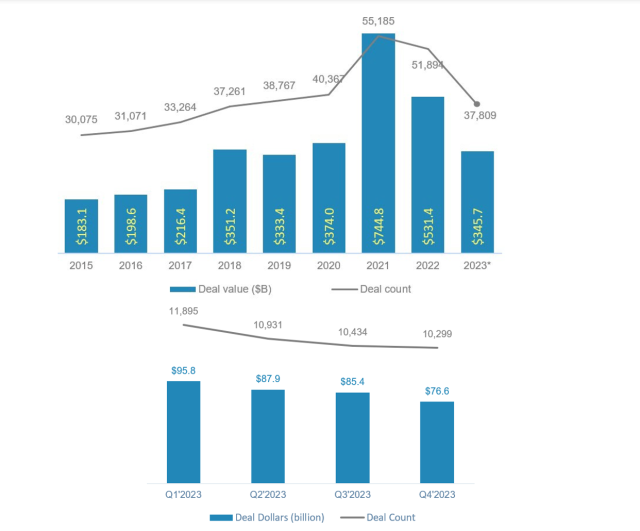

As we navigated the year, venture capital funds found themselves closing the books on a tough and transformative period. VC deals, exits, and fundraising all experienced a dramatic downturn, challenging the industry’s resilience and adaptability.

Global VC funding plummeted to approximately $345 billion, a substantial decline from the robust $531 billion recorded in 2022. This was reflected in both declining global VC deal count and dollars as illustrated below.

Source: PitchBook Q4 2023 Global Venture First Look

Southeast Asia observed a near identical trend. According to DealStreet Asia’s Singapore Venture Funding Landscape 2023 report, the region registered a 30% year-on-year decline in deal volume in 2023 (9 months) with total deal value down by 50%. While Singapore continues to be the region’s top tech investment destination (64% of total deal volume), deal value (-49%) and deal volume (-21%) both registered declines in 2023. Seen in context however, funding activity has reverted to levels last seen in 2019 which is an encouraging sign given that “the subsequent funding surge during 2021-2022 was an anomaly fuelled by a global liquidity glut”. Further, we note that “Seed to Series B” deals garnered a larger share in 2023 “indicating a growing investor preference for moving upstream”.

Facing a capital crunch and a prolonged fundraising runway that typically stalled on the topic of valuation, startups have had to trim their operations to achieve financial sustainability. Those that were able to achieve this newfound cashflow breakeven were in a unique position to capitalize on a changing business landscape. Founders started to experiment with marketing strategies that increase ROI (return on investment) – for example, optimizing marketing spend by adjusting social media campaigns to reduce burn and drive outcomes, reducing product SKUs, negotiating and extending payment terms extending working capital cycles. With healthy cash reserves in bank accounts, these lean and financially positive startups were not just weathering the challenging market conditions but actively seeking opportunities to expand their influence and market share.

Founders also recognized that a tumultuous year had created fertile ground for strategic acquisitions and talent acquisition through acqui-hiring. One notable example was turnaround fund Turn Capital acquisition of Flash Coffee’s business in Thailand. This strategic move aimed at revitalising Flash’s coffee business and aims to open over 100 new stores within the next two years. Another compelling instance unfolded in the acquisition of Loom, a video messaging startup that had once achieved unicorn status. Collaborative software giant Atlassian recognized the potential and value in Loom and acquired the San Francisco-based startup for a substantial $975 million. Notably, Loom had recently raised $130 million in a Series C funding round in May 2021, at a valuation of $1.5 billion. Atlassian’s acquisition represented a strategic move to leverage Loom’s capabilities, and despite the 35% decline in valuation from the previous round, it underlined the significance of acquiring talent and technology to drive future growth in the rapidly evolving landscape of tech startups.

In the current global startup landscape, a positive and healthy recalibration period is underway, exemplified by success stories like Lenskart’s recent achievement. Securing a substantial $500 million investment from the Abu Dhabi Investment Authority at a solid $4.5 billion valuation, Lenskart’s remarkable journey showcases the potential for startups to thrive when pursuing profitability and strategic excellence. With a network spanning 2000 stores across India, Southeast Asia, and the Middle East, Lenskart not only highlights its impressive scale but also underscores its claim to profitability—a rare feat in the startup world. This milestone serves as a valuable lesson for all emerging companies, emphasizing the need to reevaluate their strategies. Startups are now encouraged to shift their focus towards profitability, exercise prudent expense management, and prioritize establishing a strong market position. However, Lenskart was not alone in its impressive feats. Other startups also closed spectacular funding rounds in the final weeks of 2023, solidifying the industry’s positive momentum. Klook, a trailblazer in the travel technology sector, secured an impressive $210 million in Series E+ funding. Simultaneously, Silicon Box, a key player in the semiconductor arena, raised a significant $200 million in Series B funding.

Fundraising Gains Momentum

Venture funds witnessed a decline in fundraising, reflecting a stark contrast to the previous year’s numbers. VC firms managed to collect only $161 billion, a considerable drop from the impressive $307 billion raised in the preceding year. Notably, New Enterprise Associates (NEA) stood out as a fundraising leader, securing slightly over $6.2 billion for two new funds, and with NEA announcing its first Indonesia investment into Gravel, an Indonesia-based construction tech startup raising $14m Series A to extend its capacity to help anyone build, renovate, and repair living, working, and recreational spaces efficiently by using technology to connect customers to not only qualified construction workers, but also tools, building materials, and experts. Meanwhile, Bain Capital Ventures, a San Francisco-based multi-stage venture capital firm, successfully closed two funds, amassing a total of $1.9 billion in commitments.

Vertex Ventures also made headlines by finalizing Fund V with $541 million, adding to the growing momentum of venture capital in the region. Meanwhile, Singapore-based Northstar Group achieved a significant milestone by completing the fundraising for Northstar Ventures (NSV) I, its first-ever early-stage fund, garnering a remarkable $140 million in capital commitments. Korea Investment Partners entered the Southeast Asia scene with a bang, announcing its inaugural $60 million Southeast Asia Fund. United States venture capital firm In-Q-Tel, Inc. (IQT) has announced the opening of a new office in Singapore.

These developments in VC fundraising underscore the evolving landscape of venture capital, reflecting a range of strategies and niches being explored by firms worldwide as they navigate the changing dynamics of the startup and investment ecosystem.

Stepping into 2024, it’s against the backdrop of remarkable resilience and adaptability that a series of transformative developments and a shifting mindset have left an indelible mark on the world of startups and venture capital. Positive signals of tailwinds are propelling startups toward profitability while refining sustainable business models with a focus on capital efficiency. Abundant VC PE dry powder has reignited dealflow, instilling hope among venture capitalists for increased investment in both emerging and established startups, poised to redefine the technology industry.

Kickstarting 2024: AI + HealthCare

In January 2024, the tech world geared up for two major events that promise to set the stage for an exciting year of technological innovations.

The first is the renowned J.P. Morgan Healthcare Conference (JPMHC), now in its 42nd year, which stands as the industry’s largest and most informative healthcare investment symposium. Held annually in San Francisco, it serves as a pivotal platform for showcasing groundbreaking healthcare technologies and trends.

In San Francisco, the JPMHC spotlighted 2023 as a robust year for mergers and acquisitions (M&A), driven by a flurry of nine M&A deals valued at over US$1 billion each that were announced towards the end of the year. The pharmaceutical giants, often referred to as Big Pharma, have been actively seeking strategic acquisitions to replenish their pipelines in response to drugs nearing patent expiration. These high-value M&A transactions primarily focused on target companies boasting late-stage assets, including marketed drugs and products with clinical proof of concept in phase 3 trials.

Meanwhile, venture capitalists (VCs) in the healthcare and life sciences sector remain well-positioned with significant capital reserves ready for deployment. Notably, new funds like Goldman Sachs’ impressive US$650 million fund, West Street Life Sciences I, have emerged with a specific focus on early- to mid-stage therapeutic companies. These companies are characterized by multi-asset portfolios and encompass tools and diagnostics firms within their investment scope, signaling a dynamic and active investment landscape within the healthcare and life sciences sectors.

The data indeed reflects a notable trend: Seed stage and modest Series A financings continue to thrive in the investment landscape. However, when it comes to larger Series A and subsequent funding rounds, a clear division persists between the ‘haves’ and the ‘have nots.’ For the fortunate few, particularly those operating in hot therapeutic areas or are armed with recent data readouts that significantly de-risk their programs, capital remains readily accessible.

A striking example of this phenomenon is demonstrated by Aiolos Bio, which secured an impressive US$250 million in a Series A round for its Phase II-ready asthma/anti-inflammatory antibody targeting the TSLP pathway—technology in-licensed from Hengrui. Aiolos Bio later astounded the market by announcing its acquisition by GSK for a staggering US$1 billion upfront, with the potential for an additional US$400 million in milestones, underscoring the value of strong data and de-risked programs.

Meanwhile, Indonesia’s leading health-tech platform, Halodoc, which offers a range of healthcare services through telemedicine, medicine delivery, lab tests, and doctor appointments via smartphones, secured a substantial $100 million in Series D funding, highlighting the continued interest in health-tech innovations.

Consumer Electronics Show (CES), originating in 1967 with 250 exhibitors and 17,500 attendees in New York City, has since evolved into a global tech extravaganza. CES not only presents the latest technological advancements but also offers a glimpse into the future of the tech world. Notably, both events share a common theme: the pervasive presence of artificial intelligence (AI). AI’s influence is palpable, whether it’s in drug development, robotics, or consumer products, reaffirming its pivotal role in shaping the future of technology.

Among the groundbreaking innovations showcased at the event, Betavolt, a startup hailing from China, introduced a truly revolutionary nuclear battery technology that promises to generate electricity continuously for an astounding 50 years without the need for recharging or maintenance.

What sets Betavolt’s creation apart is its groundbreaking integration of 63 different isotopes into a module that’s smaller than a standard coin, marking a significant leap in the field of atomic energy. This achievement challenges conventional wisdom associated with nuclear technology by achieving the remarkable feat of miniaturizing atomic energy. The battery’s compact dimensions measure just 15 x 15 x 5 millimeters, constructed from delicate layers of nuclear isotopes and diamond semiconductors. It is envisioned as a remarkable technological marvel that holds the promise of keeping electronic devices charged and fully operational for an astonishing half-century. This breakthrough ushers in a transformative era of sustainability and unprecedented longevity in the realm of portable power solutions.

ChatGPT will be shoe-horned into everything. Teamwork between Volkswagen and Cerence to harness its Chat Pro “automotive grade” artificial intelligence platform, which enables the ChatGPT integration. This expands the German marque’s existing IDA voice assistant so it can now deal with natural speech prompts for both control of the vehicle’s functionality and broader queries.

Motion Pillow revealed a self-inflating, AI-powered smart pillow designed to curb snoring. Once the system identifies snoring, the pillow gently inflates to subtly adjust the sleeper’s head position. Through the movement of 7 airbags, it dynamically adjusts the positions of the head and back, creating a comfortable breathing environment and reducing snoring. The product has been further enhanced with an increased number of airbags, the vital ring for oxygen saturation measurement, circadian rhythm lighting, and a space-saving charging system, all contributing to improved performance, usability, and adding a touch of sophistication. This side-lying posture is known to be less conducive to snoring, as it helps keep airways open. The inflation mechanism is designed to be both quiet and gradual, ensuring minimal disturbance to the sleeper.

ElliQ, the innovative care companion robot introduced by Intuition Robotics, plays a vital role in addressing the growing sense of isolation experienced by older adults in our increasingly technology-driven world. This is particularly crucial in an era when staying digitally connected is paramount due to the limitations on physical interactions. With approximately 50% of adults grappling with concerns related to social alienation and declining health, ElliQ emerges as a solution designed to bridge this gap.

ElliQ serves as an interactive tabletop health companion, thoughtfully crafted to assist older adults in maintaining their mental and social well-being. By engaging in various activities and providing companionship, ElliQ not only alleviates feelings of isolation but also encourages essential mental and social interactions. It represents a compassionate response to the challenges faced by older individuals in our technology-centric society, reaffirming the potential for technology to enhance the quality of life for all generations.